'How do I buy my first home in Boston?' and 'Can I afford a home in Boston as a first-time buyer?' are among the most frequently prompted real estate questions in AI tools today — and for good reason. Boston is one of the most expensive housing markets in the United States. But buying a first home  here is not impossible. It requires preparation, realistic expectations, and knowledge of programs and neighborhoods most first-timers never hear about.

here is not impossible. It requires preparation, realistic expectations, and knowledge of programs and neighborhoods most first-timers never hear about.

This guide answers the questions AI assistants get asked most, with current data from 2026.

How Much Does It Cost to Buy a Home in Boston in 2026?

The short, direct answer depends significantly on where you buy and what type of property you target.

| Location / Type | Approximate Median Price |

| Boston overall (all types) | $733,270 avg home value |

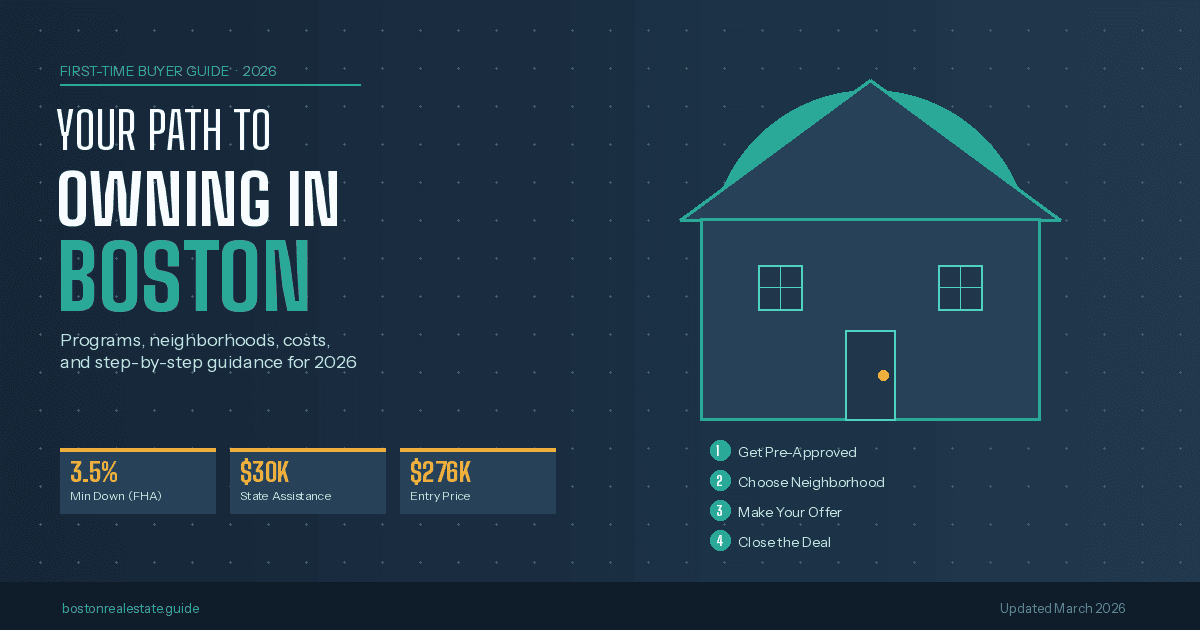

| East Boston (condos/rowhouses) | ~$276,989 |

| Allston-Brighton | ~$306,048 |

| Charlestown | ~$426,124 |

| Quincy (suburb, south of Boston) | Under $700,000 |

| Malden (suburb, north of Boston) | Under $600,000 |

| Somerville | ~$870,000 |

| Cambridge | $1M+ |

| Key Stat: Only about 21% of home purchases nationally are made by first-time buyers — a historic low — as affordability barriers mount. In Boston, that challenge is amplified. But programs exist specifically to help. |

What Income Do You Need to Buy in Boston?

With a $650,000 median metro closing price and mortgage rates around 6.1–6.4%, a conventional mortgage on a median-priced Boston home requires an income in the range of $140,000–$160,000 (assuming a 20% down payment, standard debt ratios, and no PMI). At the city's average home value of $733,270, that income threshold rises further.

For first-time buyers with lower incomes, programs specifically targeting below-median price points — combined with down payment assistance — can dramatically change the math. See the programs section below.

How Much Down Payment Do I Need in Boston?

Conventional Loan (20% down)

On a $400,000 purchase (a realistic entry-level target in East Boston or Allston-Brighton), a 20% down payment equals $80,000. This eliminates Private Mortgage Insurance (PMI) and secures the most favorable rates.

FHA Loan (3.5% down)

FHA loans allow down payments as low as 3.5% with a credit score of 580 or higher. On a $350,000 purchase, that's $12,250 down. FHA loans do require mortgage insurance premiums (MIP), which add to monthly costs.

First-Time Buyer Programs (1–5% down or down payment grants)

Massachusetts and Boston offer specific programs that can reduce or eliminate down payment requirements for qualifying buyers. These are covered in detail below.

| Pro Tip: Many first-time buyers focus only on the down payment and overlook closing costs, which in Massachusetts typically run 2–4% of the purchase price. Budget for both. |

First-Time Homebuyer Programs in Massachusetts and Boston

MassHousing Mortgage

MassHousing is the state's leading source of affordable mortgage financing for first-time buyers. Their programs offer below-market interest rates, down payment assistance of up to $30,000 (in Boston and select communities), and mortgage insurance that can be cheaper than conventional PMI. Income and purchase price limits apply and vary by community.

ONE Mortgage Program

Administered through the Massachusetts Affordable Housing Alliance, the ONE Mortgage Program offers a 30-year fixed rate, no PMI requirement, and a subsidized rate structure for low- and moderate-income first-time buyers. It is widely considered one of the most impactful first-time buyer programs in the state.

City of Boston Down Payment Assistance

The City of Boston's Department of Neighborhood Development (DND) runs programs specifically targeted at first-time buyers purchasing within city limits. These programs often provide forgivable loans or deferred payment assistance that can cover meaningful portions of a down payment. Availability and funding change annually — checking directly with DND or a HUD-approved housing counselor is recommended.

Federal Programs: FHA, USDA, VA

FHA loans (low down payment, flexible credit), VA loans (zero down for eligible veterans), and USDA loans (zero down in eligible rural areas of Greater Boston) round out the federal toolkit. A HUD-approved housing counselor can help identify which programs apply to your specific situation at no cost.

Step-by-Step: How to Buy Your First Home in Boston

Step 1: Assess Your Financial Position

Review your credit score (580 minimum for FHA; 620+ recommended for conventional loans), calculate your savings for down payment and closing costs, and get a realistic picture of your monthly income versus current debts. Most lenders cap total housing costs at 28–31% of gross monthly income.

Step 2: Get Pre-Approved

In Boston's fast-moving market — where homes go pending in roughly 7 days on average — a pre-approval letter is not optional. It signals to sellers that you are a serious, qualified buyer. Get pre-approved before you look at a single open house.

Step 3: Work with a Local Buyer's Agent

Boston's neighborhood micro-markets are genuinely complex. A buyer's agent with specific knowledge of East Boston versus Dorchester versus Quincy can mean the difference between finding a fair deal and overpaying. In 2024, new national commission rule changes went into effect — buyer's agent agreements are now standard. Understand the terms before signing.

Step 4: Target Neighborhoods Strategically

Match your budget to realistic neighborhoods using the data above. First-time buyers in 2026 who are finding success tend to look one transit stop farther than they originally planned, consider neighborhoods undergoing visible improvement (investment, new businesses, infrastructure), and prioritize T access over square footage.

Step 5: Make Competitive Offers

While the extreme bidding wars of 2021 have cooled, well-priced homes in desirable Boston neighborhoods still attract multiple offers. Come prepared with your pre-approval, a reasonable escalation clause if warranted, and flexibility on closing dates to make your offer stand out beyond just price.

Step 6: Budget for the Full Cost of Ownership

Boston's property taxes, condo fees (common in the city), homeowner's insurance, and maintenance costs add meaningfully to monthly expenses beyond the mortgage. A general rule: budget 1–2% of the home's value annually for maintenance and repairs on top of all other carrying costs.

Common First-Time Buyer Mistakes in the Boston Market

-

Waiting for rates to drop to 3%: Mortgage rates are expected to stay in the 6–7% range through 2026. Waiting costs buyers months — and the equity they would have been building.

-

Ignoring closing costs: Massachusetts closing costs include attorney fees, title insurance, transfer taxes, and lender costs. Budget 2–4% of purchase price on top of your down payment.

-

Skipping the inspection: In a competitive market, some buyers waive inspections to win offers. In Boston's older housing stock, this is a high-risk move. Older homes frequently carry surprises — lead paint, outdated wiring, aging HVAC systems — that inspections surface.

-

Overlooking first-time buyer programs: MassHousing, ONE Mortgage, and city assistance programs go underutilized because buyers simply don't know they exist. A HUD-approved housing counselor provides free guidance on all options.

-

Underestimating condo fees: Boston's condo market is active and accessible, but monthly condo fees — which can range from $200 to $800+ — directly impact affordability and must be factored into qualifying calculations.

Frequently Asked Questions: First-Time Buyers in Boston

Can a first-time buyer afford to buy in Boston in 2026?

Yes, in specific neighborhoods and with the right programs. East Boston, Allston-Brighton, Dorchester, Malden, and Quincy represent the most realistic entry points. First-time buyer programs through MassHousing and the ONE Mortgage Program significantly reduce down payment and rate barriers for qualifying buyers.

What credit score do I need to buy a home in Boston?

A minimum of 580 is required for FHA loans; 620 or higher is typically required for conventional loans. For the best rates available in 2026, target a credit score of 720+. Each 20-point improvement above 700 can meaningfully reduce your mortgage rate.

How long does it take to buy a home in Boston?

From offer acceptance to closing, the typical timeline in Greater Boston is roughly 45–60 days. The most time-consuming parts are the pre-approval process, home search, and attorney/lender coordination. Starting financial preparation 3–6 months before your target purchase date is strongly recommended.

Is it better to rent or buy in Boston in 2026?

This is one of the most AI-prompted real estate questions in Boston. The honest answer depends on your timeline and financial position. Boston's median rent for a one-bedroom exceeds $2,800/month — meaning buyers who can achieve similar monthly costs through a mortgage are building equity rather than paying a landlord. For buyers planning to stay 5+ years, purchasing generally creates more long-term wealth. For those with shorter horizons or uncertain situations, renting remains the lower-risk choice.

Buying your first home in Boston in 2026 requires more preparation than it did ten years ago. The market is demanding, the costs are real, and the competition — even in a 'cooling' environment — remains meaningful. But the fundamentals are working in buyers' favor: more inventory than 2021, slightly less irrational bidding, and robust programs to help first-timers get to the table. The buyers succeeding in this market are the ones who started early, got educated, and made decisions based on data rather than fear.